ether.fi Cash Card

Got crypto but no way to spend it? Or better yet, want to spend it without actually selling it? That's exactly what the ether.fi Cash Card is for. In this ether.fi review, we'll look at why this crypto card is different from the rest of the market.

The ether.fi Cash Card is a non-custodial card accepted at all merchants where VISA is accepted (over 100 million locations). Your crypto stays under your control in the ether.fi Vault – ether.fi never holds it directly. The card supports Google Pay and Apple Pay, so you can add it to your phone. 3D Secure support is also a given. Thanks to its non-custodial architecture, this crypto card is safer than cards from centralized exchanges.

Privacy

I founded this website to educate people about digital privacy. So you might be wondering, what does a card that requires KYC have to do with that? Just like I wrote in my article How to Surf Without a Trace about fingerprinting – life is a compromise. In my opinion, the ether.fi Cash Card reveals only the bare minimum about you and everything else stays hidden. Let's take a look at what that means and how the card actually works.

First, for comparison with a standard bank debit card: "A regular bank knows every step you take. It sees your salary, knows how much you have in savings, and knows exactly what you spend it on. All this information forms your financial fingerprint, which the bank can share with authorities or advertising companies.

The bank has the complete picture. ether.fi only sees a slice – your card spending. The difference is like someone seeing one photo from your life versus having access to your entire photo album. Ether.fi sees one piece of the whole mosaic.

A crypto card with Borrow Mode (described below) breaks this chain. Yes, when you pay at a store, Visa knows that a card with a certain number spent 50 EUR. But Visa and the card issuer don't see your entire financial life. They don't see your salary, they don't see your savings, and most importantly – they don't know where the crypto backing the card came from. In borrow mode, you become just someone who took out a loan to the card issuer. No income tracking, no spending profiling, no connecting the dots into your personal profile.

What ether.fi offers is privacy – not anonymity.

Privacy means your bank doesn't know how much crypto you have. Privacy means Visa doesn't see your salary. Privacy means advertising companies don't have access to your financial profile. That's what ether.fi provides.

How ether.fi Cash Card Works

This crypto card can operate in two different modes: Direct pay mode and Borrow mode, which is unique among cards available on the market. Below I'll describe how these two modes work.

Direct pay mode

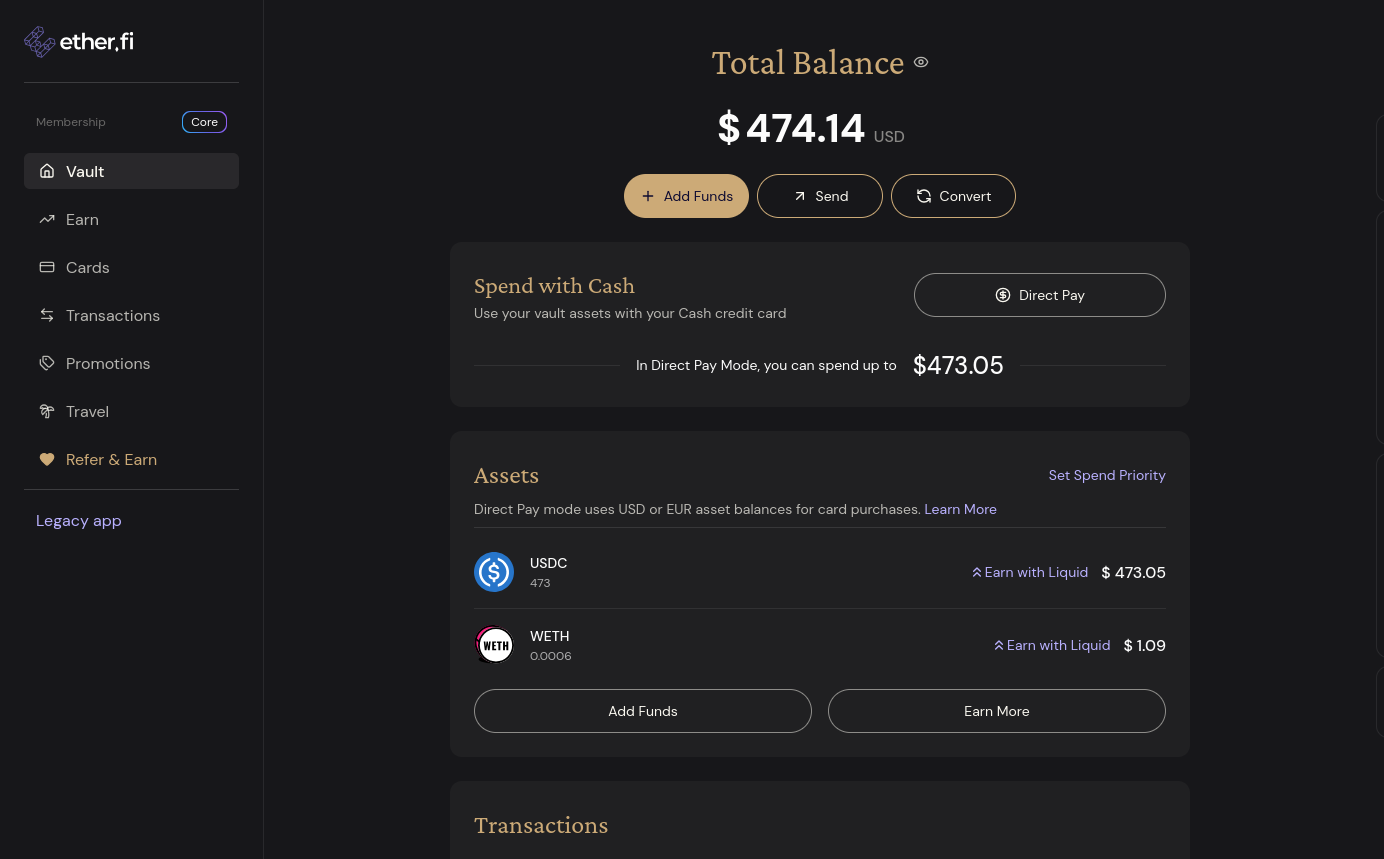

Direct Pay mode basically works like a crypto debit card. In Direct Pay Mode, funds are deducted directly from your Vault (from USDC/EURC). Essentially, at the moment of transaction, your stablecoins are converted to fiat right at the point of payment. It's the simplest way to pay with crypto at regular stores.

Direct Pay is ideal if you hold stablecoins and want a simple off-ramp to fiat. It's not dramatically different from competitors like the Coinbase Card, but the main difference is the non-custodial architecture – your money sits in a smart contract that you control, not in a centralized exchange's hot wallet. This mode doesn't generate any interest or debt. It's suitable for everyday payments and situations where you want simplicity.

Let me add what ether.fi sees in this case:

- It sees how much USDC you have in your Vault

- It sees how fast you top up

- It sees your spending

But even here, there's separation from traditional banking:

- ether.fi doesn't know where that USDC in your Vault came from (if you sent it from a wallet not linked to your identity)

- Your bank doesn't know these funds exist

- No traditional financial institution sees the whole chain

Fig.1: ether.fi card dashboard in Direct pay mode

Borrow mode

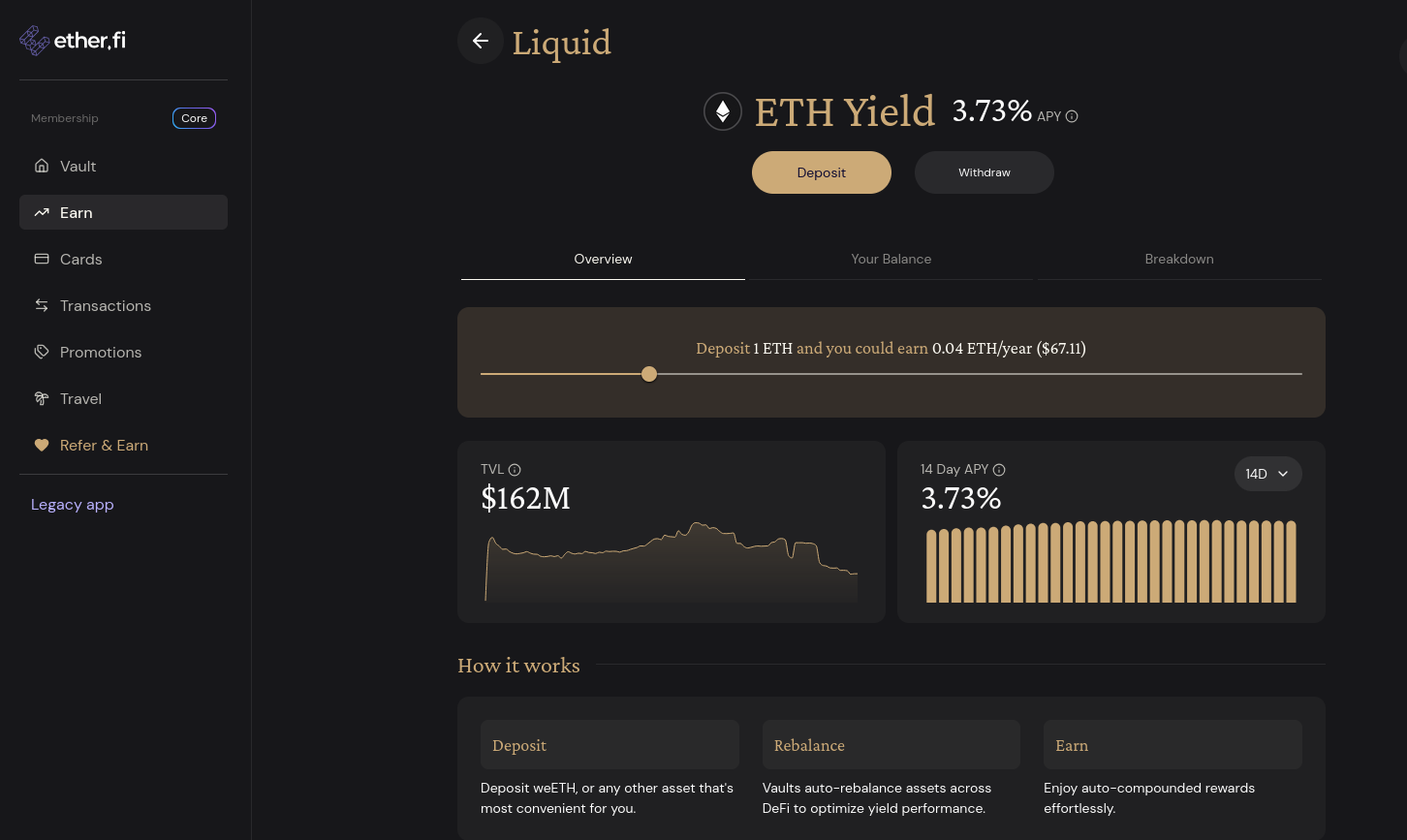

In short – a loan that's almost free. In Borrow Mode, you don't sell your crypto, you borrow against it, using it as collateral (e.g., staked ETH/weETH). Your ETH stays in the Vault and continues to generate staking rewards. You can pay with crypto without actually selling it.

This crypto-backed loan has no fixed repayment term. When you spend 100 USD, you create a 100 USD debt. Whenever you have free stablecoins (USDC) in your ether.fi Vault in the future, you can simply use them to reduce or pay off the debt. You can keep the debt open for months or years, as long as your collateral is high enough.

Interest is not calculated on your entire collateral, but only on what you actually owe. It's calculated every second and added to your debt. If you have a debt of 100 USD, you pay about 4 dollars per year in interest. If you don't spend anything, the debt is 0 and you pay nothing.

Liquidation risk (Watch out for this)

This is the main catch. Because there's no repayment term, ether.fi guarantees its money by holding your ETH as collateral.

If you borrow a lot and the price of ETH drops sharply, the value of your collateral drops too. If the collateral value falls below a certain threshold (the so-called Loan-to-Value ratio), ether.fi will automatically sell (liquidate) your ETH to cover your debt.

Example: You have 1 ETH (let's say it's worth 3000 USD). You borrow 1000 USD. If ETH drops to 1200 USD, the platform sells your ETH, takes its 1000 USD + interest, and sends the rest back to you.

Understanding staking on ether.fi

When you stake ETH on ether.fi, you get back tokens that you can further use. That's the main advantage over traditional staking.

What exactly do you get?

When you stake ETH, you receive one of these liquid staking tokens (LST):

| Token | What it is | APY |

|---|---|---|

| eETH | Ether.fi's own liquid staking token | ~3.73% |

| weETH | Wrapped eETH (represents your stake + rewards) | ~2.38% |

| weETHs | Symbiotic version (additional yield layer) | ~3.50% |

What can you do with these tokens?

These tokens aren't just "paper" – they're fully functional:

- Borrow Mode – You can use them as collateral for a loan against stablecoins

- DeFi – You can use them in other protocols (Aave, Uniswap, etc.)

- Trading – You can sell them on exchanges

- Transfer – You can send them to another wallet

Why is there weETH in the vault and not ETH?

Because your 1 ETH is no longer in the vault. The moment you staked it, a conversion happened:

1 ETH → staking → 1 eETH → wrap → 1 weETH

weETH is proof that you own that ETH.

Why is this actually such an advantage?

The money to repay has to come from somewhere eventually. So what's the trick compared to just selling your ETH right away?

A. Tax optimization

When you sell ETH, a taxable event is immediately triggered (of course, it depends on your tax residency). But if you borrow against it, no taxable event occurs.

B. Interest vs. Staking yield (Yield offset)

This is where the magic happens that makes the loan almost free:

You pay 4% interest on the loan. But your ETH, which you used as collateral, still generates staking rewards (often 3–4% APY). Your ETH appreciates and pays you yield that covers the cost of the loan interest. The resulting "price" for having money available is then minimal (e.g., 1% per year).

Is it "almost free"? Almost, but not quite. Here's the math:

| Item | Value |

|---|---|

| Staking rewards from eETH | ~3–4% APY |

| Loan interest | 4% APY |

| Net cost | ~0–1% APY |

Practical example

- You send ETH to ether.fi and stake it

- ETH is locked on a validator and earns yield

- You receive weETH as a receipt token

- You use weETH as collateral

- You spend USDC from the debt pool

- 4% APY interest accrues per second

- You repay the debt by sending USDC to the vault

Fig.2: Yield display on the ether.fi platform

C. You keep future gains

When you sell ETH, you lose it. If ETH shoots up 100% in a year, you get none of that. In Borrow Mode, you still hold that ETH. If it goes up, your collateral is higher and you can borrow even more without selling a single ETH.

Summary

Borrow Mode isn't free. It's a loan with 4% interest that you have to repay eventually (e.g., from your bank salary or by selling other crypto). But it gives you the ability to spend the value of your ETH today while still holding that ETH, with staking generating yield that largely covers the interest.

Cashback

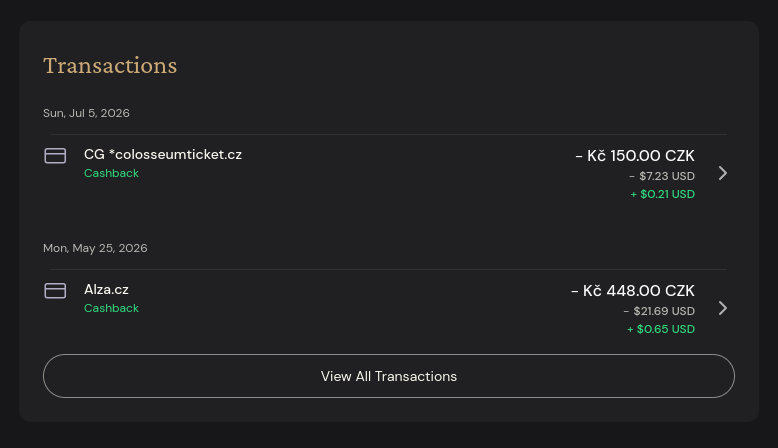

Basic principle

Cashback is a program that rewards you for using the ether.fi Cash Card for everyday purchases. Rewards are credited automatically – you don't need to activate or claim anything. Cashback is paid in crypto, specifically in wETH (Wrapped Ethereum), and is automatically deposited into your vault monthly. The standard base rate is 3% cashback on purchases.

EUR transactions and FX

EUR transactions have an adjusted cashback rate – ether.fi offers 0% FX fees for EUR payments, and cashback is reduced to compensate for this benefit.

Fig.3: Cashback display on the ether.fi Cash Card

TIERS

Tier overview and requirements

| Tier | Requirement – Staking | Requirement – Points | Daily limit |

|---|---|---|---|

| Core | Free (no staking) | Default | ~$30,000 |

| Luxe | 15,000 ETHFI | 10,000 points/month | ~$50,000 |

| Pinnacle | 100,000 ETHFI | 50,000 points/month | ~$100,000 |

| VIP | Invite-only | Invite-only | Not public |

How to earn points?

- 3,000 points for every $1,000 spent

- Points are calculated monthly, tier is updated automatically

- If you use ETHFI staking, you get the tier immediately and stably (without monthly point tracking)

Benefits of each tier

Core (free)

- Cashback: 3% on the first $2,000 monthly, then 1% up to $3,000, 0.5% above $3,000

- Cards: 3 virtual + 1 physical (plastic or with deposit)

- FX fee: 1% (except EUR, where it's 0% FX)

- Onramp: $10,000/month for 0.2% fee

- Apple Pay / Google Pay

- Annual fee: $0

Luxe (15,000 ETHFI or 10k points/month)

- Cashback: 3% on the first $10,000 monthly (instead of $2,000)

- Cards: 5 virtual cards

- Physical card: Metal (metallic purple)

- Lounge access: Airport lounge access

- Hotels: Discounts up to 65%

- Priority support

- All Core benefits with increased limits

Pinnacle (100,000 ETHFI or 50k points/month)

- Cashback: 3% up to $50,000 monthly

- Cards: 10 virtual cards + 2 physical

- Daily limit: Up to $100,000

- Business features: Suitable for entrepreneurs and corporate expenses

- Highest public tier with maximum limits

VIP (invite-only)

- Cashback: Non-public rates (likely higher than 3%)

- FX fee: 0% on all currencies

- Concierge: Personal assistant for crypto deals

- Bespoke yield strategies: Tailored investment strategies

- Exclusive events: Access to conferences, sporting events

Important limits

- Maximum cashback: $1,000/month (applies to all public tiers)

- EUR transactions: 0% FX, but lower cashback rate (compensating for the benefit)

- Unstaking penalty: If you unstake below the minimum, you return to Core and returning to a staking tier is possible only after 30 days.

Prohibited Jurisdictions

The service is not available in the following countries and regions (as of 2026).

Countries:

Belarus, Bangladesh, China, Cuba, Estonia, Finland, Hungary, India, Iraq, Israel, Nepal, Netherlands, North Korea, Philippines, Russia, Syria, Turkey, Ukraine, Venezuela, Vietnam.

U.S. States

Arizona, Delaware, Georgia, Idaho, Louisiana, Maryland, Mississippi, Missouri, Montana, Nevada, New Mexico, North Dakota, Ohio, Oregon, Rhode Island, South Dakota, Tennessee, Vermont, Washington, Wisconsin.

What I see as disadvantages

- 1% FX fee on transactions in currencies other than USD/EUR – for European users, this means the effective cashback is 2%, not 3%

- Liquidation risk in Borrow Mode if the collateral value drops

- Not available in some U.S. states (as of 2026)

- Phishing risk: There are fake websites mimicking ether.fi – always access only from the official website

Conclusion

This ether.fi review shows that the ether.fi Cash Card isn't just another crypto card. It's a tool that lets you live off crypto without selling it. 3% cashback in wETH, non-custodial architecture, and Borrow Mode that saves you on taxes – no one else currently offers this. If you hold ETH and want to actually use it, this crypto card is a must-have.

If you're interested in how to surf the web without a trace, read my article about the Mullvad browser. And if you want privacy-focused AI that doesn't track you, check out my article about Venice.ai.